How Central Bank Intervention Affects The Forex Market

Using intervention in currency strategically allows central banks to maintain stability in their national financial systems. These actions can dampen excessive swings, restore investor confidence, and prevent abrupt disruptions in trade and capital flows. The timing and scale of interventions are crucial, and unexpected moves can sometimes generate short-term market turbulence.

Central bank interventions are not limited to direct buying or selling of currency. They may involve communication strategies, adjustments to interest rates, or open market operations to reinforce the intended effect. By carefully calibrating these measures, monetary authorities aim to guide exchange rates toward desired levels without creating long-term distortions.

What is the intervention of currency?

Currency intervention, also called foreign exchange intervention, refers to actions by a country’s central bank (or sometimes its government) to influence the value of its national currency in the FX market. Unlike ordinary open-market operations aimed at domestic interest rates, currency intervention specifically targets the exchange rate by using financial operations or policy signals. Interventions come in a few forms:

Direct intervention

The central bank directly buys or sells currencies using its foreign exchange reserves to push the domestic currency up or down. For instance, Japan’s central bank bought yen (selling U.S. dollars) in September 2022 to strengthen a weakening yen. Conversely, a bank might sell its own currency (buying foreign currency) to weaken it. Direct interventions immediately affect market supply and demand for the currency.

Indirect intervention

The central bank uses policy tools or verbal guidance rather than outright FX trades. This can include changing interest rates, adjusting capital controls, or issuing forward guidance and warnings (“jawboning”). These measures influence investor expectations and capital flows, which in turn affect the exchange rate.

For example, raising interest rates can attract foreign capital and strengthen the currency, while lowering rates tends to weaken it. In May 2024, South Korea chose an indirect route by expanding a $35 billion swap line for its national pension fund (so it could obtain U.S. dollars without selling won in the market), thereby easing pressure on the won without heavy direct intervention

Central banks typically intervene to stabilize the currency when it moves too rapidly, to steer the exchange rate toward a level that supports economic policy, or to signal the market about their stance. Such actions can be unilateral or coordinated among multiple countries. In global crises or when currency moves are extreme, central banks of major economies have even cooperated on joint interventions (for example, the G7 nations jointly intervened to weaken a sharply rising yen in 2011 after Japan’s earthquake).

Objectives of foreign exchange intervention

Central banks engage in foreign exchange intervention for several reasons:

- Stabilizing the currency. Smoothing excessive volatility helps maintain economic confidence, as rapid swings in exchange rates can disrupt trade, investment, and planning. Interventions dampen sharp moves to provide a predictable environment, prevent panic, and allow markets time to adjust.

- Controlling inflation. Intervention can influence import prices. A stronger currency makes imports cheaper, helping reduce domestic inflation, while preventing excessive depreciation avoids spikes in costs for essentials like fuel and food. Currency management indirectly stabilizes inflation pressures.

- Supporting exports and competitiveness. A weaker currency can make exports cheaper and more competitive globally. Export-driven economies intervene to prevent their currency from appreciating excessively, protecting sectors like manufacturing and tourism. For example, Switzerland has historically intervened to curb an overvalued franc.

- Maintaining financial stability. During speculative attacks or financial stress, central banks act as buyers to absorb selling pressure and prevent a currency collapse. Interventions signal that authorities will not allow one-way bets, deterring speculative excess and ensuring orderly market functioning.

- Correcting misalignments. When exchange rates deviate from economic fundamentals due to speculation or temporary factors, central banks may adjust rates to reflect balance of payments, purchasing power parity, or other fundamental measures. This helps maintain alignment with the economy’s underlying conditions.

- Trade-offs and policy credibility. Not all central banks pursue all objectives simultaneously, as goals can conflict. For instance, weakening a currency to boost exports may worsen inflation if imports become more expensive. Market response is stronger when interventions are consistent with broader monetary policy and economic fundamentals, enhancing credibility.

How currency intervention affects FX markets

Currency intervention affects the FX market both mechanically and psychologically, causing immediate movements and shaping trader expectations.

- Market supply and demand. Direct intervention changes the currency’s supply-demand balance. Selling domestic currency increases supply and lowers its price, while buying reduces supply and raises its value. For example, Japan spent ¥9 trillion ($68 billion) in September 2022 buying yen, strengthening it 3–4% in two days. Sudden interventions create imbalances that traders quickly arbitrage into new rates.

- Volatility control. Central banks intervene to reduce extreme fluctuations. Acting as major buyers or sellers can stabilize the currency temporarily. Russia, in July 2025, increased daily FX sales by ₽9.76 billion ($124 million) to counter a 45% rouble surge, which helped shrink wild swings. Such actions act as counterweights to disorderly market moves.

- Influencing trader sentiment. Intervention signals influence trader behavior. Even verbal cues (“jawboning”) can reduce speculative pressure. Switzerland spent over CHF 90 billion in H1 2020 to cap franc gains, prompting investors to scale back bullish positions. Similarly, in mid-2025, RBI signaled action against excessive rupee moves, temporarily stabilizing it without actual reserve usage. Interventions shape expectations, often causing pre-emptive market alignment.

- Interest rate expectations. Indirect intervention via policy rates affects currency through capital flows. Rate hikes attract foreign investment, strengthening the currency, while cuts may weaken it. Emerging-market central banks (e.g., Turkey, Argentina) have used rate adjustments to defend currencies alongside direct FX actions. Asian central banks may prefer FX reserves or capital controls over rate changes to maintain domestic focus. Consistent messaging across interventions and rates enhances credibility.

- Short-term vs. long-term effects. Interventions often produce immediate exchange rate shifts but may not alter long-term trends driven by fundamentals. A one-off action buys time or corrects overshoots but cannot reverse persistent trends caused by interest rate gaps, growth differentials, or trade imbalances. Japan’s 2022 yen-buying intervention halted a slide briefly, but U.S.–Japan rate differentials eventually resumed downward pressure, highlighting that fundamentals dominate long-term outcomes. Sustained effect requires policy shifts or successful market psychology changes.

Effectiveness of central bank interventions

The success of central bank interventions depends on several factors:

- Market conditions. Interventions have more impact in thin or illiquid markets or during off-peak hours, as large orders sway prices more easily. Surprise after-hours interventions can catch traders off-guard. In highly liquid markets, even large interventions may be absorbed quickly. One-way speculative momentum can reduce effectiveness, while interventions aligned with sentiment reversals or overshooting markets work best. Timing and tactical execution (stealth vs. announced) are also crucial.

- Coordination and signaling. Coordinated interventions involving multiple central banks send a strong signal and amplify impact. For example, the G7’s joint intervention in March 2011 successfully weakened the yen. Interventions seen as representing broad policy consensus gain more traction. Unilateral actions may be less sustainable if other major players disagree. Clear communication is vital; explicit or implicit commitments from credible central banks often achieve half the desired effect, as traders respect their track record and resources.

- Policy credibility and consistency. Interventions must align with broader monetary policy. Inconsistent actions, such as tightening one tool while loosening another, undermine market confidence. Credible interventions are backed by sustainable reserves and consistent policy. For instance, the Swiss National Bank’s franc cap at 1.20 per euro worked for years due to virtually unlimited capacity, while the Bank of England’s attempt to defend the pound on Black Wednesday 1992 failed because reserves and political support were insufficient. The “longer wallet” principle shows that central banks capable of enduring prolonged interventions gain more respect.

- Underlying economic fundamentals. Interventions are most effective when they reinforce fundamental trends. Defending a currency aligned with economic strength, current account surpluses, or positive interest rate differentials is easier. Attempts against weak fundamentals (high inflation, deficits, slowing growth) usually fail and become costly. Successful interventions often coincide with turning points in fundamentals or sentiment. The ECB intervened sparingly (2000 and 2011) because the euro was significantly misaligned; these actions were effective as they resonated with fundamental trends. Artificially defending a currency contrary to fundamentals risks exploitation by speculators.

- Strategic timing and credibility. Central banks achieve maximum effectiveness when they choose opportune moments: thin markets, aligned policy, and necessary exchange rate correction. Adequate reserves and market trust enhance credibility. Poor timing or misalignment with fundamentals may result in large expenditures with minimal lasting effect.

Interventions can temporarily stabilize or redirect currency movements, but long-term effectiveness depends on market conditions, coordination, policy credibility, and alignment with fundamentals. Central banks succeed when interventions complement underlying economic trends and leverage credibility, rather than attempting to fight speculative forces or fundamentals.

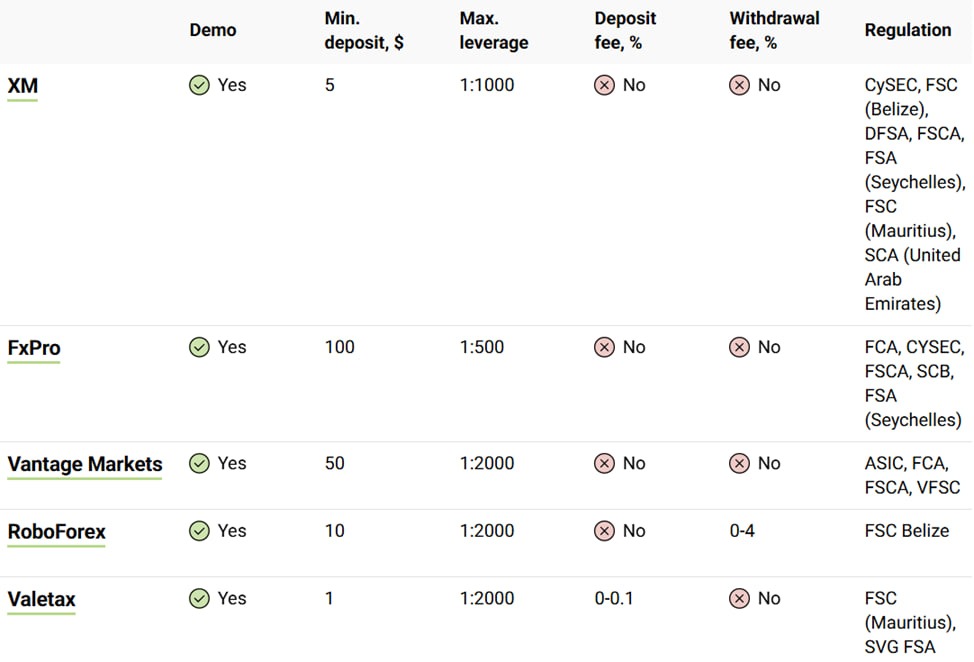

Looking to trade the moves sparked by central bank interventions? Start with a broker that’s regulated in your region, offers tight spreads and fast execution, and makes deposits/withdrawals hassle-free. Below are the best Forex brokers to invest and trade on; pick one that fits your budget, platform preference, and support needs.

Risks and limitations

While currency interventions can be beneficial, they also carry risks:

- Market distortion. Frequent interventions can lead to misaligned exchange rates, affecting trade balances.

- Resource constraints. Sustained interventions may deplete foreign exchange reserves.

- Inflationary pressures. Unsterilized interventions can increase the money supply, leading to inflation.

- Retaliation. Other countries may view interventions as competitive devaluations, potentially leading to trade disputes.

Conclusion

Currency intervention remains a powerful instrument for managing exchange rate stability and achieving broader macroeconomic goals. Whether direct or indirect, the methods chosen by central banks reflect national priorities and available resources. Traders must stay alert to signals of potential interventions, understand their impact on market liquidity, and assess them in the context of inflation, interest rates, and geopolitical developments. By tracking recent policy shifts and historical precedents, both novice and advanced participants can better navigate the foreign exchange market.

Post a comment